The VSME standard (Voluntary ESRS for non-listed Small- and Medium-sized Enterprises) becomes the central basis for voluntary sustainability reporting in small and medium-sized enterprises (SMEs). It sets a clear cap for sustainability information that companies subject to CSRD reporting requirements may demand in their upstream and downstream value chain. This makes the VSME standard relevant for all SMEs that wish to voluntarily provide sustainability information or develop a sustainability strategy. Be it for enquiries from banks (where there may be a need to supplement the VSME content), large companies with a CSRD obligation or for communicating their own sustainability strategy.

For many SMEs that have already prepared for the European Sustainability Reporting Standards (ESRS) and are now likely to be exempt from the reporting obligation as a result of the first omnibus regulation, the VSME standard offers the opportunity to continue utilising the previous results and collected data in a meaningful way. It is based on the central principles of the ESRS, but enables a more flexible and resource-saving implementation. In this article, we provide an overview of the basics of the VSME standard, highlight the parallels and differences to the ESRS and explain how companies can utilise the individual scope for design in the VSME standard for their own sustainability reporting.

Contents

- The new role of the VSME standard

- The VSME standard: An introduction

- From the ESRS to the VSME standard - similarities and differences

- Utilising the scope of the VSME standard in reporting

- Conclusion

The new role of the VSME standard

Changes in reporting obligations due to the draft of the first omnibus regulation of 26 February 2025

On 26 February 2025, the EU Commission presented the draft of the first omnibus regulation, which provides for significant changes to the Corporate Sustainability Reporting Directive (CSRD). One of the key changes concerns the postponement of the reporting obligation for companies that are currently subject to the CSRD by two years - i.e. until the 2027 reporting year. However, the change to the scope of the CSRD itself is more far-reaching:

- Companies with fewer than 1,000 employees and a net turnover of less than 50 million euros or a balance sheet total of less than 25 million euros will no longer be subject to the CSRD reporting obligation in future.

- A so-called "value chain cap" or "protective shield" is also being introduced: Companies that still fall under the CSRD reporting obligation can request a maximum of the information contained in a voluntary standard from non-reporting business partners with fewer than 1,000 employees. This is to be issued by the European Commission on the basis of the VSME in the form of a delegated act. Changes to the VSME standard are therefore possible.

It is important to note that the first omnibus regulation of 26 February 2025 is a draft. It still has to go through the European legislative process. For this reason, amendments are still possible. In addition, the changes to the EU directives still have to be transposed into national law.

We regularly report on the latest status and current developments in our newsletter.

[glossary_exclude]Methods and best practice for sustainability in your mailbox

Significance of the changes for SMEs that are exempt from the reporting obligation

This means for many small and medium-sized companies: The extensive preparations for CSRD reporting and the requirements of the ESRS will no longer be mandatory. Many SMEs have already carried out a materiality analysis, collected data and set up processes for sustainability reporting. The challenge now is to continue to utilise this effort in a meaningful way. We can say in advance: the effort was not in vain.

This is where the VSME comes into play. This voluntary reporting standard was developed by the EFRAG (European Financial Reporting Advisory Group) to offer SMEs a practical and simplified option for sustainability reporting. EFRAG submitted the standard to the EU Commission in December 2024. It is currently only available in English. The VSME was mentioned several times in the draft of the first omnibus regulation and its role in voluntary sustainability reporting was emphasised.

The VSME standard: An introduction

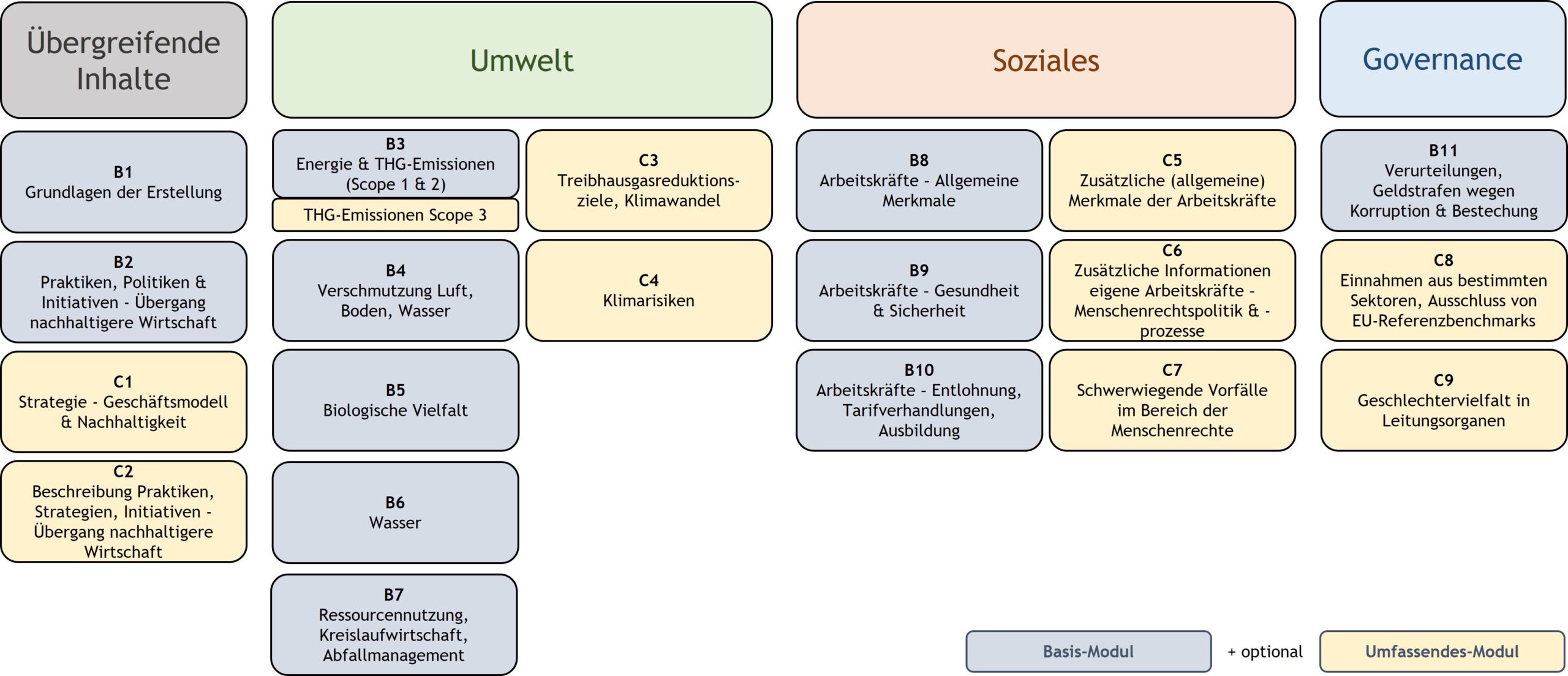

The VSME standard has a modular structure and offers two main modules. The basic module and the comprehensive module. Depending on their individual requirements and resources, companies can decide whether they want to use only the basic module or a combination of the basic module and the comprehensive module. In our opinion, this flexibility makes it easier for SMEs to organise their sustainability reporting according to their specific situation.

The basic module

This module focuses on basic sustainability metrics and information. It covers areas such as:

- General informationThe basics of reporting and presentation of strategies, concepts, goals and future initiatives as part of a transition to a more sustainable economy.

- Environmental indicatorsData on energy consumption and greenhouse gas emissions, environmental pollution, biodiversity, water consumption, resource utilisation and waste management.

- Social key figuresInformation on the workforce, including general characteristics, health and safety, remuneration, collective bargaining and training.

- Governance key figuresInformation on convictions and fines in connection with corruption and bribery.

The comprehensive module

For companies that want to provide more detailed insights, primarily on the topic of climate and their own employees, this module offers extended reporting requirements, including

- StrategyDescription of the business model and sustainability-related initiatives.

- Environmental indicators: Setting targets to reduce greenhouse gas emissions, climate risk assessments and transition strategies.

- Social key figuresAdditional information on the workforce, human rights policies and processes, and serious adverse human rights incidents.

- Governance key figures: Information on sales in certain sectors, exclusions from EU reference benchmarks and gender diversity in management positions.

Both modules combine to form the following structure.

Structure of the VSME standard (Source: Own presentation)

From the ESRS to the VSME standard - similarities and differences

Even though the VSME is significantly smaller (66 pages) than the ESRS (287 pages), there are many parallels to the ESRS. Our assessment is that anyone who is familiar with the ESRS will quickly find their way around the VSME. This is accompanied by the great advantage of being able to easily transfer previous results and use them for reporting in accordance with the VSME standard.

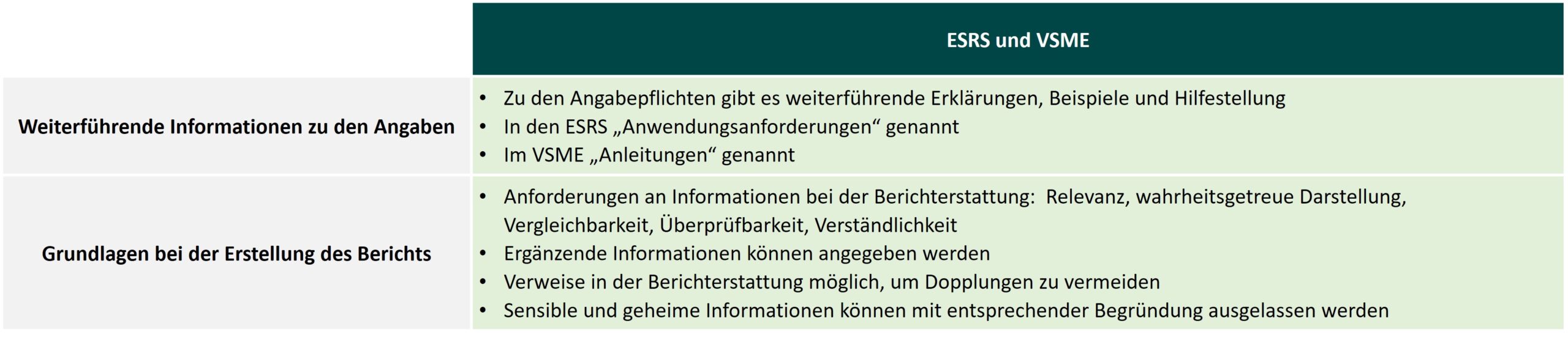

The similarities between the VSME standard and the ESRS

As a streamlined version of the ESRS, the VSME shows parallels to the ESRS both in terms of content and structure. These are illustrated graphically in the following diagram.

Similarities between the ESRS and the VSME standard (Source: Own presentation)

In addition to the similarities, there are differences to the ESRS.

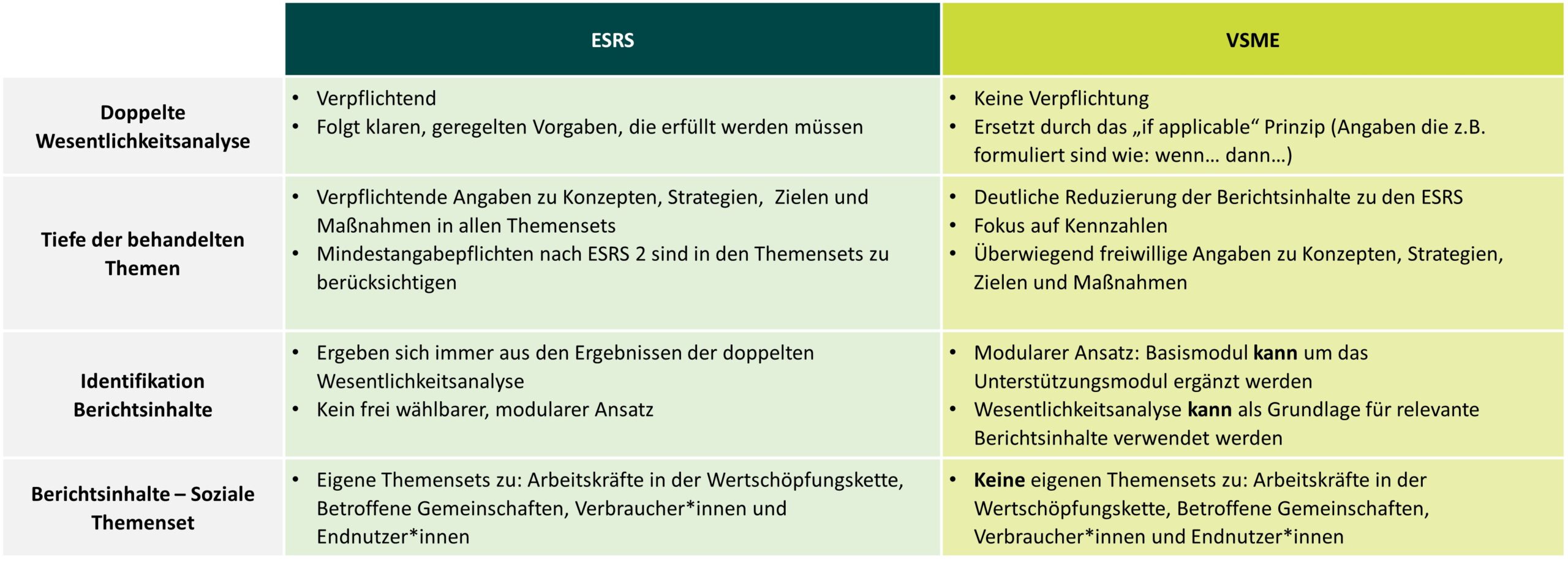

The differences between the VSME standard and the ESRS

Firstly, there are purely formal differences between the two standards. Because the VSME standard is voluntary, there is no audit requirement. This is in contrast to the CSRD report, which must be audited as part of the management report in Germany. There are also differences in the content of the two standards.

Differences between the ESRS and the VSME standard (Source: Own presentation)

Utilising the scope of the VSME standard in reporting

The differences between the VSME standard and the ESRS show the flexibility in reporting. While the ESRS sets strict guidelines, the VSME standard gives companies more freedom in the design of their sustainability reports. This allows the standard to be optimally adapted to individual company requirements. Two specific application examples show how the VSME standard can be used in a targeted manner.

Provide targeted key figures with the VSME standard

As already mentioned, the VSME standard defines clear limits for sustainability information that companies subject to CSRD may request from SMEs in their value chain. By implementing an indicator-orientated VSME standard, companies can optimally prepare for these requirements and provide relevant data in a structured manner.

Furthermore, the VSME standard can be flexibly expanded to include additional key figures that are requested, for example, by capital providers such as banks or investors. This makes it a valuable tool for transparent and targeted communication of the sustainability status to these groups.

Utilising the freedom of the VSME standard for an individual sustainability strategy

Companies that have already carried out a double materiality analysis as part of CSRD reporting can utilise the results in a targeted manner for the further development of their sustainability strategy. The insights gained into material impacts, risks and opportunities are helpful here.

Thanks to the freedom of the VSME standard, companies can flexibly organise their sustainability strategy. Topics can be prioritised according to urgency or impact. The focus can then initially be on these issues, for which targets and measures can be developed in order to specifically reduce negative effects, increase positive effects, minimise risks and make the best possible use of opportunities.

The key figures in the VSME standard are not only used for reporting purposes, but are also a valuable tool for managing and monitoring defined sustainability targets and measures that are part of the sustainability strategy. This targeted use makes the company's progress measurable.

If initial concepts, strategies, targets or measures are already available as a result of the preparation for CSRD reporting, these can be integrated directly into the report in accordance with the VSME standard. Key figures that have already been collected can also be adopted.

With the VSME standard, this process takes place at the individual pace of the reporting companies - without rigid specifications, but with the possibility of approaching sustainability strategically and effectively.

Conclusion

The VSME standard offers small and medium-sized enterprises a voluntary alternative to comprehensive reporting in accordance with the European Sustainability Reporting Standards (ESRS). It enables SMEs to build up sustainability data or continue to utilise existing data in a meaningful way and to prepare specifically for enquiries from banks, companies subject to CSRD reporting requirements or their own sustainability communication.

Thanks to its modular structure, the VSME standard gives companies the freedom to customise the scope of reporting - in stark contrast to the ESRS. At the same time, it creates a standardised structure that companies can use as a guide and supplement to suit their individual needs.

For SMEs that have already familiarised themselves with CSRD reporting and the ESRS but are now exempt from the reporting obligation, the switch to the VSME standard is a logical step.

[glossary_exclude]

Are you planning the next steps towards sustainability?

Ask me for a free information meeting.

I am ready with advice and pleasure.

Michael Jenkner

Sustainability strategy and reporting topics

One comment

Comments are closed.