Companies usually define KPIs (Key Performance Indicators) for their strategies and associated goals. Sustainability KPIs or sustainability indicators are in turn important tools for monitoring and measuring a company's sustainability performance. In order to measure sustainability and use it effectively and efficiently on an ongoing basis for corporate and sustainability goals, we recommend six steps for companies, which we describe in this blog post.

Contents

- Determine key sustainability issues

- Develop sustainability goals for the company

- Defining sustainability KPIs and measuring sustainability

- Check data availability and quality

- Continuously measuring sustainability

- Communicate sustainability goals and KPIs

- Conclusion

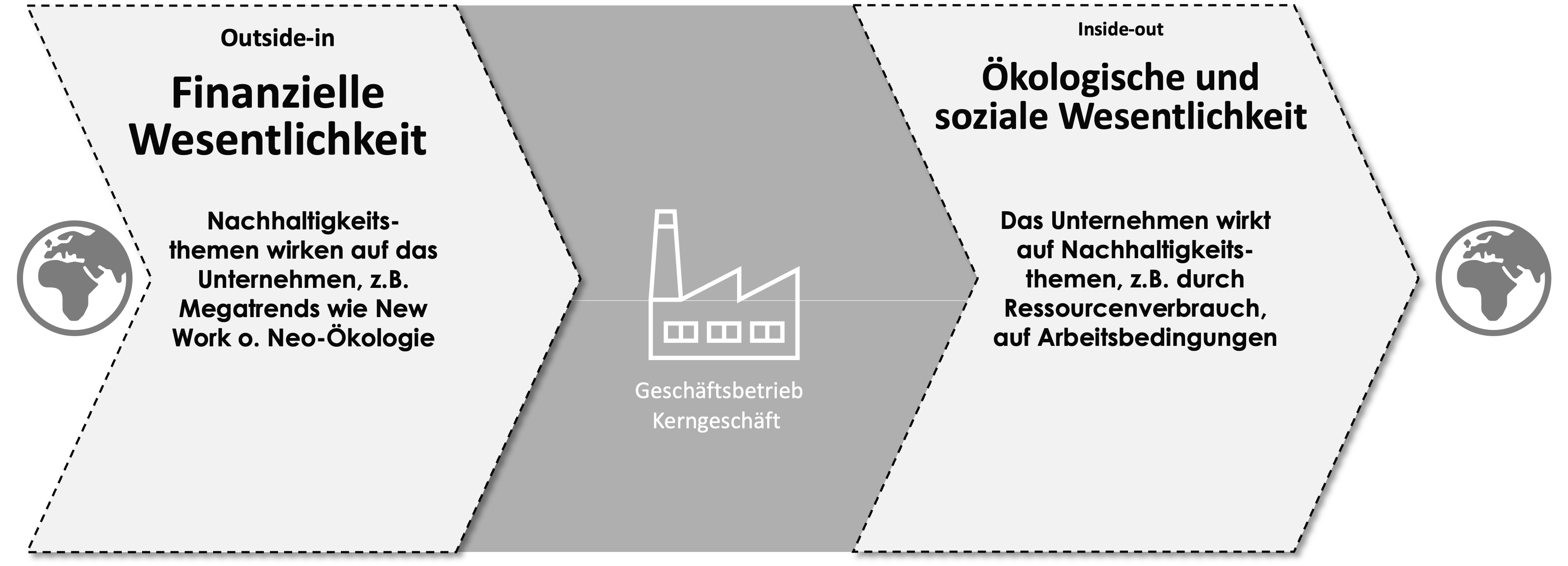

1. determine key sustainability issues

Fig.: Identification of material sustainability topics according to CSRD / ESRS (own illustration)

- The company identifies the Material sustainability issues that have an external impact on the company (outside-in) (see figure above). These can be developments affecting society as a whole, such as demographic change, or megatrends such as new work and neo-ecology (cf. Future Institute). Other external factors can be of an industry- or company-specific nature, e.g. CO2 pricing or supply bottlenecks from service providers. They are business relevant for companies, hence the term Financial materialityin German Financial materiality (cf. CSRD- and ESRS-regulation)

- The company identifies the material sustainability issues on which it has an external impact (inside-out). These depend on the company and industry. Key issues for a manufacturing company can be, for example, the consumption of resources such as raw materials, water, energy and solvents. These topics have social, ecological and economic effects, which is why they are also referred to as Impact Materialityin German Materiality of the impact (cf. CSRD- and ESRS-regulation)

- Traditionally, the identified sustainability issues are evaluated and the sustainability issues classified as material are then summarised in a sustainability report. Materiality matrix (see illustration below). Material sustainability topics per industry can also be found via the SASB, the Sustainability Accounting Standards Board, which develops accounting standards for sustainability and is linked to the International Financial Reporting Standards (IFRS). The SASB has identified material sustainability topics for 77 sectors; we recommend using these as a minimum variant for a materiality assessment: https://www.sasb.org/standards/materiality-finder/?lang=de-de

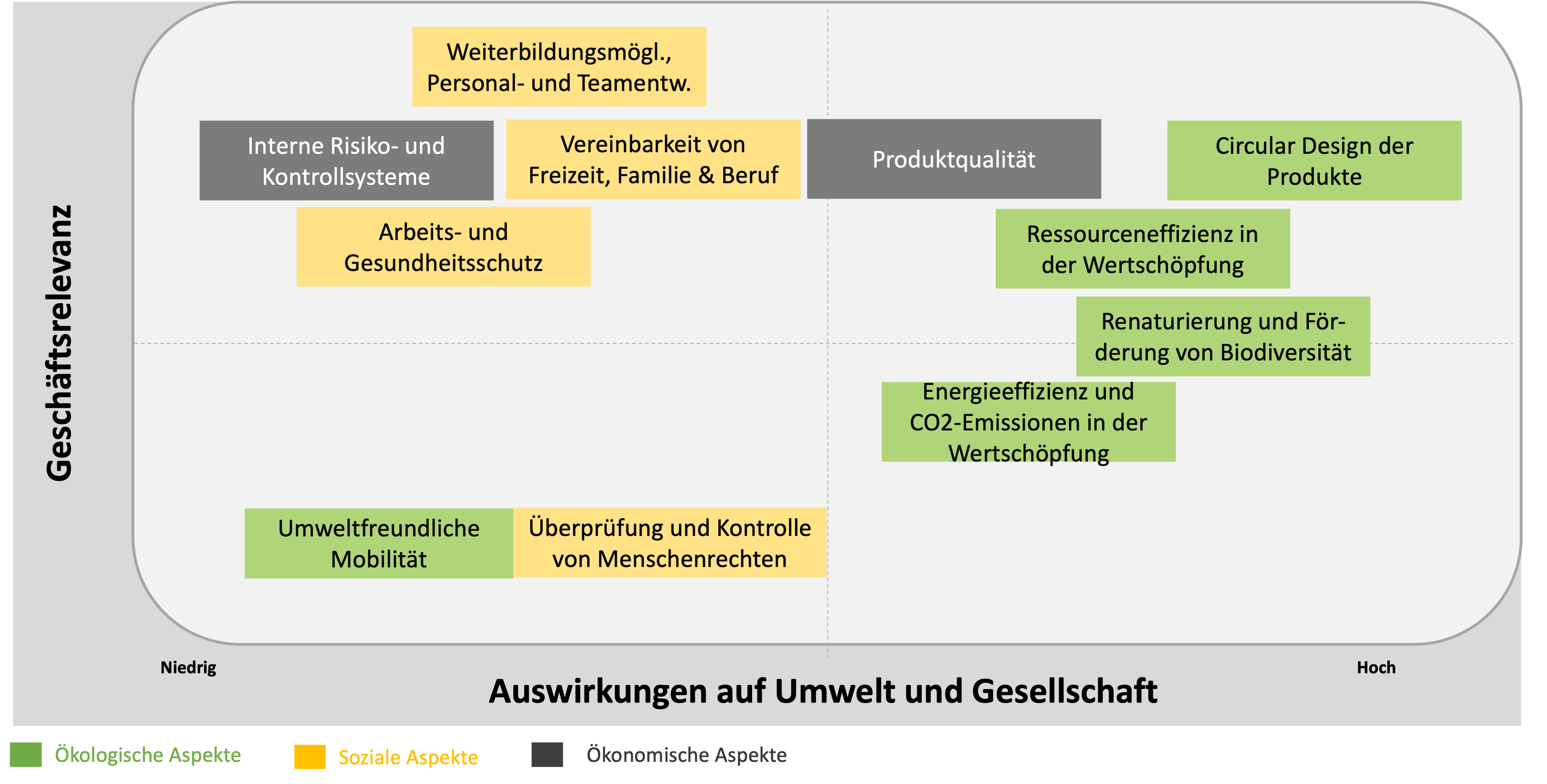

Fig.: Example materiality matrix for a company (own illustration)

2. develop sustainability goals for the company

- The company Defines goals for the key sustainability issues and anchors these in a strategy (to our blog article Building a sustainability strategy).

Examples of sustainability goals

Here are some Examples of sustainability goalsthat companies can pursue:

- Economic objectives (on profitability, governance, compliance, management):

- Improving customer satisfaction

- Regular review of sustainability targets and KPIs and regular updating of the sustainability strategy

- Establishment of internal risk and control systems

- Reducing the risk of cyber attacks

- Social objectives (on social and corporate social issues and human rights in the supply chain):

- Increase in employee satisfaction

- Introduction of an individual training programme for each employee

- Improving occupational health and safety (initial and follow-up certification in accordance with ISO 45001)

- Improving workplace ergonomics

- Improving respect for human rights in the supply chain

- Ecological goals (on environmental topics):

- Reduction of resource consumption

- Reduction of CO2 emissions

- Increasing the reuse of packaging materials

- Introduction of a take-back system for products at the end of their life cycle

3. define sustainability KPIs and measure sustainability

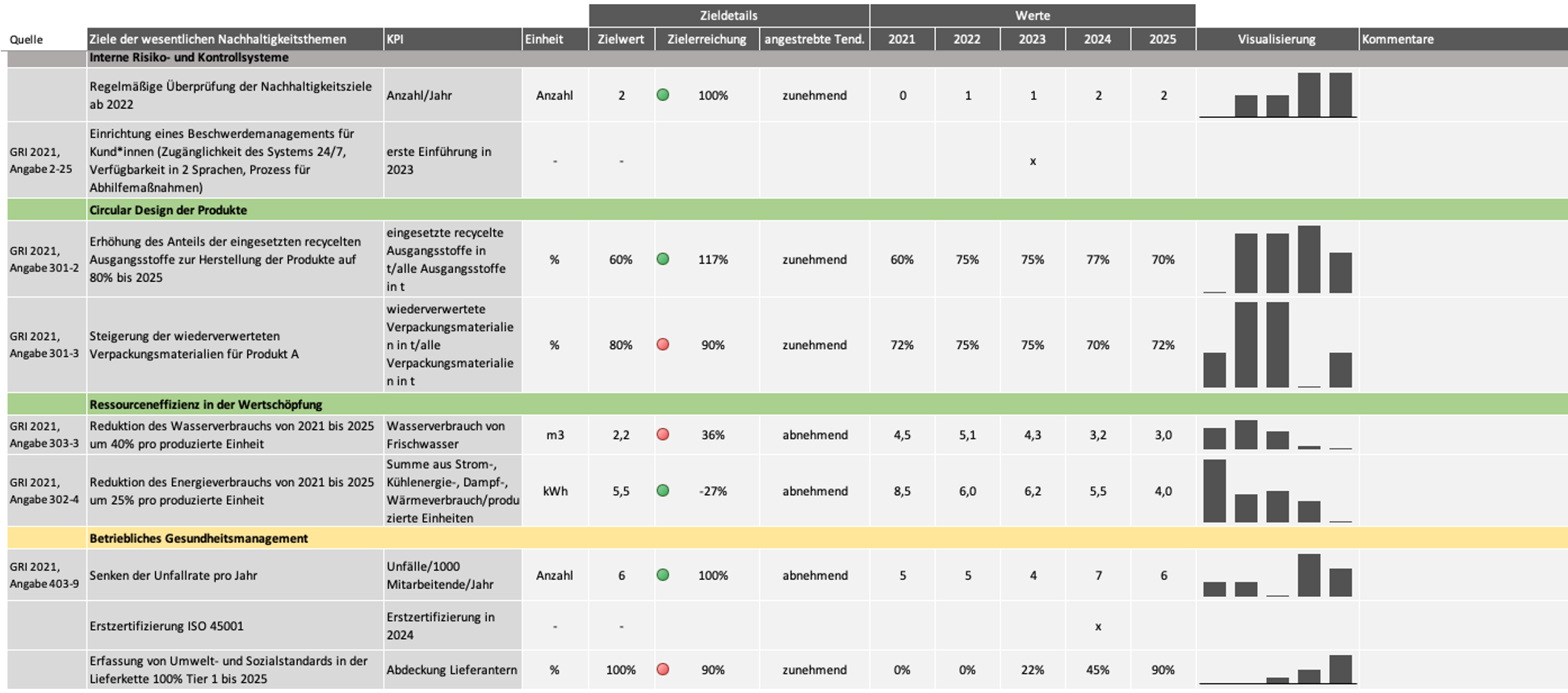

- Once you have defined your key sustainability topics and sustainability goals, you can now Define KPIs. These help to measure the progress of sustainability. This is best done in addition to each other, i.e. sustainability targets are identified for the key sustainability issues, which in turn are measured using sustainability KPIs. (see figure below, example of an Excel management tool or sustainability dashboard)

- Prioritise your KPIs. It is important to have a limited number of KPIs to ensure that the organisation is tracking the most important metrics and focusing on the most relevant targets.

How to define sustainability goals SMART?

Sustainability goals should SMART be specific, measurable, attractive, realistic and time-bound. This means

- specificGoals should be formulated as concretely as possible.

- Measurable: Each goal should be determined qualitatively or quantitatively in order to be able to measure sustainability.

- attractive: If you, your employees or others who are necessary to achieve the goals are behind them, you will push the goals within reach.

- realistic: Consider the feasibility within the given time with given means.

- terminated: KPIs should have a defined target time, i.e. a date by which the specified target should be achieved.

Examples of sustainability KPIs

Here are some Examples of sustainability KPIsthat companies can pursue:

- Economic sustainability KPIs

- Number of customer complaints

- EU taxonomy-compliant turnover: Proportion of net sales that originates from products or services that are linked to the EU taxonomy. EU taxonomy are compliant

- OpEx: Proportion of operating expenses that comply with the EU taxonomy

- CapEx: Proportion of current or future capital expenditure that complies with the EU taxonomy

- Scope of IT-related outages

- Click here for economic sustainability KPIs for every company and every industry.

- Social sustainability KPIs

- Employee satisfaction

- Diversity quotas, e.g. proportion of women in management positionsn

- Fluctuation rate

- Number of human rights complaints Accident and injury rates

- Number of training hours per employee

- Click here for social sustainability KPIs for every company and every industry.

- Environmental sustainability KPIs

- Proportion of recycled raw materials used in the manufacture of products

- Creation of renaturalised areas in m2

- Total greenhouse gas emissions in kilograms of CO2 equivalent

- Share of renewable energy sources in total energy consumption

- Total energy consumption in kWh

- Total water consumption in m3

- Waste in tonnes

- Amount of packaging waste per unit produced in g

- Click here for environmental sustainability KPIs for every company and every industry.

Excel management tool or sustainability dashboard for key sustainability topics, sustainability targets and sustainability KPIs (own illustration)

4. check data availability and quality

- When defining the KPIs, also check your data sources. How is the database or the Data availability? Do you already have the KPIs or do they need to be collected from scratch? Is the data quality medium to high based on measured values and calculations or are only estimates available so that the data quality should be improved in subsequent years?

- Is the Data quality If the assumptions and estimates are not available to the extent necessary, we recommend that they be carefully documented in order to minimise expenses in subsequent years.

Examples of data sources for sustainability KPIs

Here are some Examples of data sourcesfrom which their sustainability KPIs can originate:

- Economic data

- Market and financial data from accounting, controlling, business development department

- Kandend data from the CRM (e.g. by means of customer surveys, complaints and feedback on products and services)

- Operating data from IT, production and operating processes (e.g. process times, reject rate, machine utilisation, etc.)

- Governance and compliance data from the legal department

- Investment data from the purchasing or procurement department

- Social data

- Employee data from personnel management (via personnel files, employee surveys, staff turnover, etc.)

- Company health management (e.g. accident rate, long-term sickness, etc.)

- Supply chain data from the purchasing or procurement department through to the legal department

- Ecological data

- Data on purchased energy, water and other resources, operating materials, etc. from purchasing

- Data on employee mobility from HR management, on business trips from the travel department, on the vehicle fleet from purchasing or the procurement department

- Data on transport volumes from the logistics department

- Data on the use and disposal of sold products and services from the development and R&D department

Are you planning the next steps towards sustainability?

Ask me for a free information meeting.

I am ready with advice and pleasure.

Franziska Kramer

Sustainability strategy and reporting topics

5. continuously measure sustainability

- The company regularly measures the targets on an ongoing basis using the selected KPIs. (to our blog article Overview of sustainability KPIs) Monitoring, e.g. in controlling, ensures that sustainability targets and KPIs are still relevant and contribute to achieving the company's goals and sustainability strategy.

- If the results do not meet expectations, the following can be Corrective measures be taken.

- On the other hand, have corporate and sustainability goals changed in the meantime? Updatedthe sustainability KPIs may also need to be adjusted.

- We also recommend reviewing the sustainability targets and KPIs at regular intervals. to be updated.

6. communicate sustainability targets and KPIs

- The company communicates the sustainability targets and KPIs to relevant stakeholders, also known as stakeholder groups or interest groups. We recommend the different interests of the stakeholder groups in communication into account. It helps if you gain an overview of the stakeholder groups and their expectations and goals in order to be able to address the groups specifically via storytelling. (to our blog article How sustainability communication works)

- Principles for communication are, among other things, that the content is presented transparently and honestly, is attractively presented and is simple and easy to understand. Ideally, comparability can be established in order to present the company's added value in comparison to competitors.

Examples of data sources for stakeholder groups and their expectations

Here are some Examples of stakeholder groups and their expectations:

- Investors: They are primarily interested in economic and financial key figures and how sustainable the business model is and how it shapes the market.

- Customers: They are primarily interested in consumer aspects such as prices, product quality, delivery times and, as studies show, increasingly also in ecological and social aspects. These can therefore be used as a means of differentiation and competitive advantage over competitors.

- Employees: They are particularly interested in working conditions, opportunities for co-determination, further training and career paths, team building, remuneration and equal opportunities. Here, too, we are seeing a growing trend of employees paying more attention to the social and environmental aspects of their company and wanting to identify with their work in their private lives in terms of their values and for a good cause. Sustainability is therefore also becoming a differentiating factor in the competition for skilled labour.

- Legislators: They are interested in compliance with environmental, social and governance legislation, e.g. as part of the CSR-RUG or, in future, the CSRD. Examples of laws in the area of social sustainability for which KPIs may be relevant are the Working Hours Act (ArbZG), the Occupational Health and Safety Act (ArbSchG), the Minimum Wage Act (MiLoG) and the General Equal Treatment Act (AGG). Examples of laws in the area of environmental sustainability in which KPIs may be relevant include the Closed Substance Cycle Waste Management Act (KrWG), the Federal Immission Control Act (BimSchG), the Federal Energy Efficiency Act (EnEfG 2023) and the Federal Nature Conservation Act (BNatSchG).

7. conclusion

Overall, selecting the right KPIs is a critical step for companies to measure their performance and achieve their goals. By defining SMART sustainability targets and sustainability KPIs and continuously implementing, updating and updating them effectively and efficiently, companies can measure and improve their sustainability performance and contribute to the success of their corporate goals.

[glossary_exclude]