Many companies ask themselves how they can measure their climate impact and create a carbon footprint for their organisation. This can actually become a challenge if data is not collected and the expertise is not available. Excessive demands and the complexity of tasks and companies can quickly cause initial motivation to fizzle out.

The good news is: In this blog post, we'll show you a structure that any company can use to create a carbon footprint. Welcome to our step-by-step guide to a company's footprint.

Table of contents

- 1. prepare the CO2 balance in the company

- How do you create good conditions for successful CO2 balancing?

- Starting sustainability as a topic in the company

- Check competitors and customer requirements

- Risk analysis as a decision-making basis for measuring the carbon footprint

- Legitimisation and consensus of the management

- Identify CO2 balance targets in the company

- Set process standard for a CO2 balance in the company

- Communicate plans

- How do you create good conditions for successful CO2 balancing?

- 2. define system limits for the CO2 balance in the company

- 3. collection and calculation of data for the company's carbon footprint

- Conclusion

1. prepare the CO2 balance in the company

How do you create good conditions for successful CO2 balancing?

Starting sustainability as a topic in the company

An essential prerequisite for a successful carbon footprint in companies is that climate protection or even sustainability is already an issue. This requires internal (and possibly even external) communication. In this way, acceptance of the relevant tasks and responsibilities can be created. In addition, awareness of sustainable development is created within the company. In the next step, motivation and training are on the agenda: every activity, every measure, every goal can only be achieved if there are people who are motivated and capable of implementing it. We write about how to sensitise and empower employees for sustainability in the blog article Creating motivation for sustainability in the company.

Check competitors and customer requirements

It is also exciting to analyse competitors' climate activities in order to understand where your own company stands in comparison to the benchmark in terms of climate protection. A simple yes/no assessment can help:

Checklist:

- Individual climate protection measures

- Climate strategy or

- Climate report or CO2 balance

In addition, customer requirements need to be reviewed, for example to determine whether customers are asking for climate-relevant data or even demanding it as mandatory.

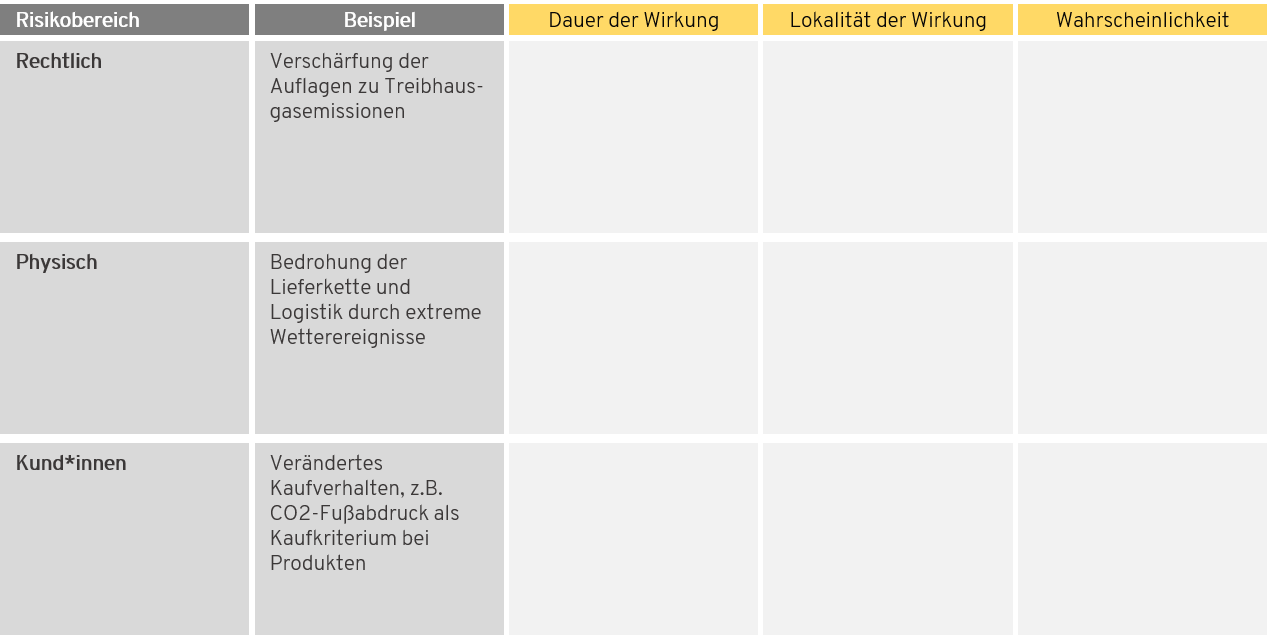

Risk analysis as a decision-making basis for measuring the carbon footprint

A risk analysis can also be a good preliminary step before drawing up a carbon footprint for a company. What climate risks and potentials exist for the company and what potential risks could arise? What consequences do the risks have for the company? Is the impact likely to be local or global and short or long-term? The risk analysis can be carried out with little effort using simple matrices. They categorise the risks into, for example, physical risks, such as the threat to the global supply chain from extreme weather events, or regulatory risks, such as the tightening of EU emissions trading regulations, according to criteria such as the duration of the impact, location of the impact, probability and frequency of the risk. The risk analysis can therefore create transparency about the necessity, reasons and objectives for carbon accounting. In addition, it provides initial indications as to which areas of the company may harbour particularly high risks or potential that need to be taken into account in the scopes.

Legitimisation and consensus of the management

Another important prerequisite for the successful creation of a carbon footprint in companies, as for any other measure, is (economic) legitimisation. Without the go-ahead from management, even the most committed endeavours come to a standstill. The effort involved must be matched by a benefit. For smaller companies in particular, carbon accounting is only practicable if it can be carried out at a reasonable cost. It therefore makes sense to scrutinise why and to what extent the footprint should be measured. Why does carbon footprinting make sense and does it have an appropriate cost-benefit ratio? If the objectives of a carbon footprint are clear in the company, the hoped-for benefits become clear and can be weighed up against the effort involved.

Identify CO2 balance targets in the company

The targets are derived from the analyses of competition, customer requirements and risks, as the analyses show how important or even mandatory a carbon footprint is for the company. Is the footprint used more for internal management or external competition? Is the calculation intrinsically or extrinsically motivated? If legal requirements or customers demand a carbon footprint, it quickly becomes clear that it is mandatory and must be carried out for extrinsic reasons. Intrinsic goals can be to analyse and reduce your own emissions and contribute to achieving the global climate targets for 2030.

Set process standard for a CO2 balance in the company

Once the company has made the decision to prepare a carbon footprint, it should be considered whether or which official standard should be used to calculate the footprint. For non-reporting companies, this is not mandatory and the calculation can be done without a standard. However, it does have advantages, such as credibility and transparency for customers, investors and others. Stakeholdersbut also compatibility and comparability with the benchmark. The use of an official standard is therefore recommended even for small companies that are not required to report. For example, the internationally recognised Greenhouse Gas Protocol. Also the DIN EN ISO 14064 is a recognised standard for calculating the CO2 footprint. Companies can carry out their calculations according to this standard and have them checked and certified by TÜV.

Communicate plans

We recommend communicating the plan to create a carbon footprint within the company internally. This does not require a major process. For example, a short time slot in a company meeting or communication by email or newsletter is sufficient. The advantages are obvious: employees feel involved and have the opportunity to ask critical questions. This increases the acceptance and motivation of support in the carbon footprinting process. This is particularly advantageous when collecting and collating data, which often involves several employees.

Depending on the scope, the company can (later) also communicate the project externally, e.g. by means of a declaration in favour of climate protection or anchoring it in the company's mission statement.

Are you planning the next steps towards sustainability?

Ask me for a free information meeting.

I am ready with advice and pleasure.

Franziska Kramer

Sustainability strategy and reporting topics

2. define system limits for the CO2 balance in the company

What are the system limits within which the company should measure emissions?

Understanding system boundaries

But what does it mean to record emissions? Which areas of the company should be considered in the carbon footprint, at what point in time and to what extent should which emissions be included? So where are the boundaries, the so-called system boundaries? By system boundaries, we mean which areas of the company and the Value chain should be included in the accounting and which should not. For example, it can be determined that only one of three raw material supply chains is included because this is probably where the most emissions are generated.

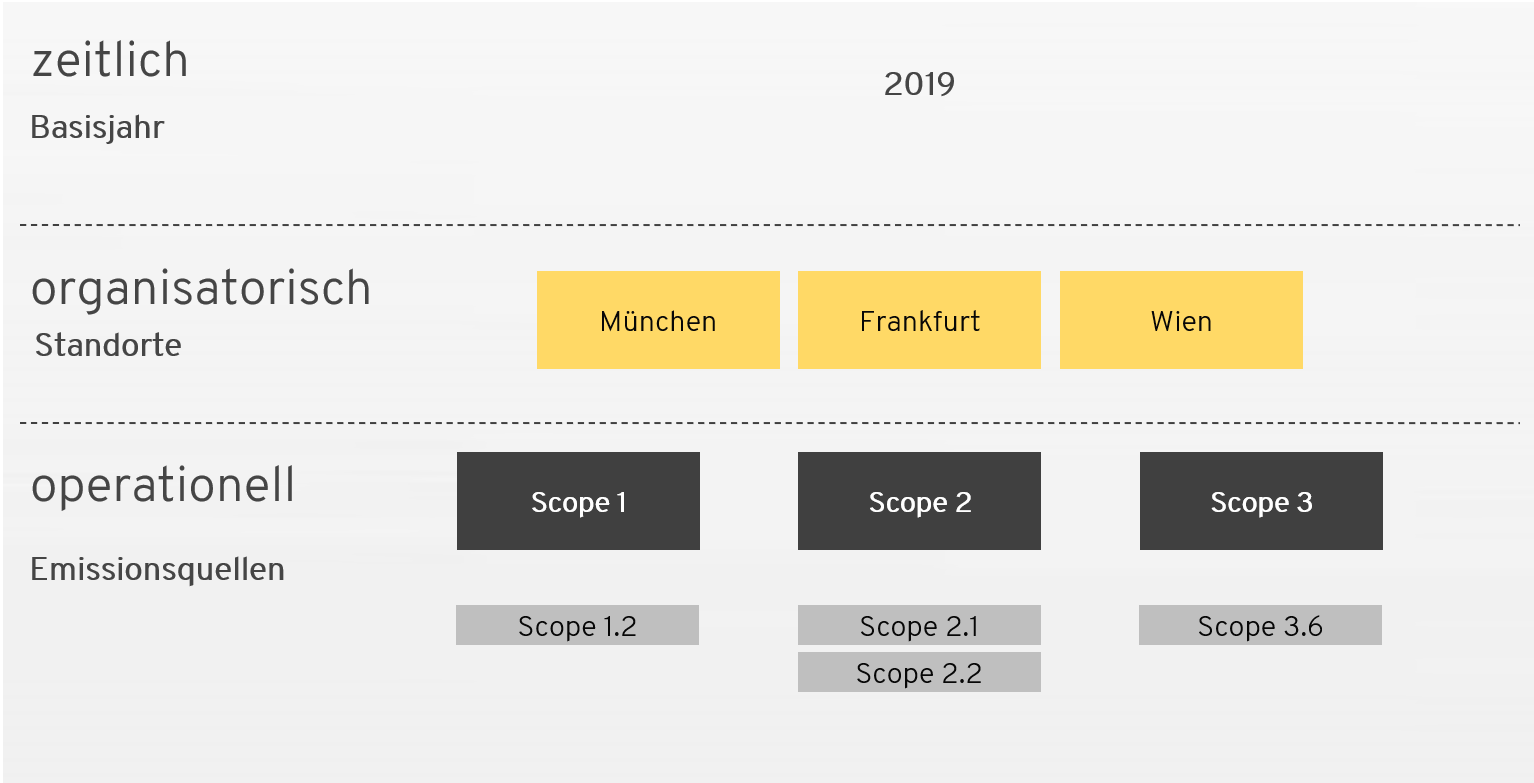

It is essential to define system boundaries so as not to end up with chaotic data collection and analysis. System boundaries are of a temporal, organisational and operational nature.

Set system time limit = base year

The period determines when the emissions are to be recorded. In most cases, emissions are collected for a period of one year and then compared with the following years. A rolling average is also possible for a survey over many subsequent years. It is important to define a base year for the company's carbon footprint. To do this, the company should choose a normal, average year with no extraordinary business events or major disruptions in the course of business (such as corona, mergers, sale of business divisions).

Determine organisational system boundaries = locations

Which locations and subsidiaries should the company include in the carbon footprint? This system limit is easy to define for smaller companies with simple ownership structures. The answer to this question is more complex for larger companies with many locations and different legal forms and ownership structures. Here, a decision must be made as to the extent to which the emissions of the specific locations are included in the carbon footprint on a percentage basis. For this purpose, either the equity share approach, the financial control approach or the operational control approach is chosen. (more on this in the Greenhouse Gas Protocol)

Define operational system boundaries = emission categories

Understanding operational system boundaries

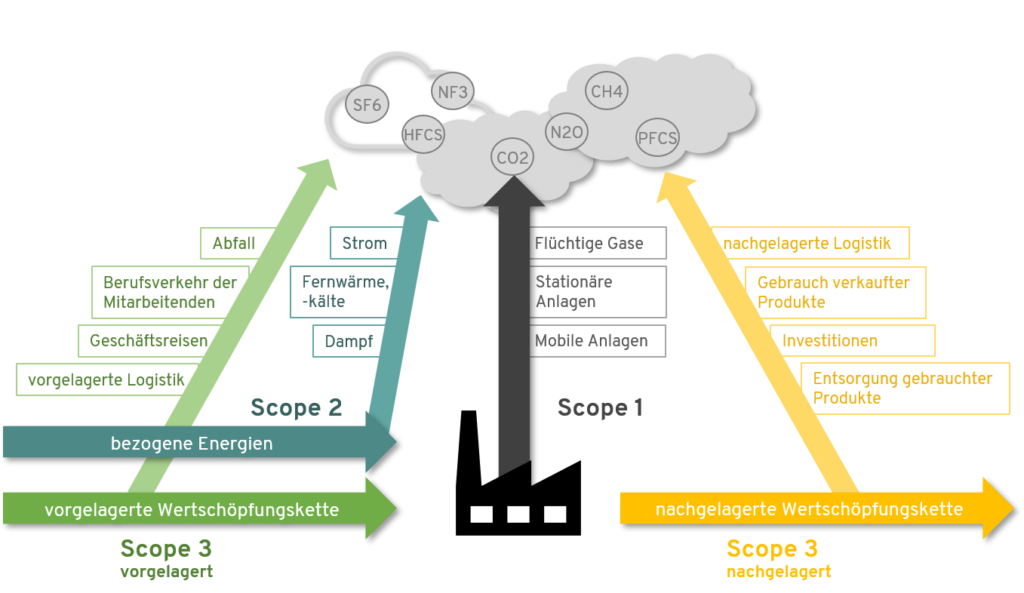

The operational system boundaries are defined in the Greenhouse Gas Protocol is defined. Emissions are usually categorised into scopes 1, 2 and 3. In the following, we present the scopes in order to make them tangible and understandable:

- Scope 1 (mandatory): Direct emissions from sources directly controlled by the company:

- Combustion in stationary systems (e.g. heating systems)

- Mobile combustion (e.g. vehicle fleet)

- Leaks (e.g. air conditioning systems)

- Scope 2 (mandatory): Indirect emissions resulting from combustion for the provision of electricity, heat or steam.

- Scope 3 (optional): Emissions that the company causes but does not control, e.g.

- Upstream value chain, such as purchased goods and services, employee mobility or waste generation

- Downstream value chain, such as transport, use, further processing and disposal of sold products

Operational system limits: Mandatory and voluntary calculation

Scope 1 and Scope 2 are mandatory to report according to the Greenhouse Gas Protocol, unless there are no or only negligible emissions in these categories (in this case, this must be justified at best). In addition, the categories in Scope 3 are not mandatory to report. Here it is important to consider which categories should be meaningfully included in the company's carbon footprint. It is best for the company to weigh up this decision according to which emissions it expects in which areas and the effort involved in obtaining the data. Specifically, this means that categories with high emissions and therefore high relevance should be included.

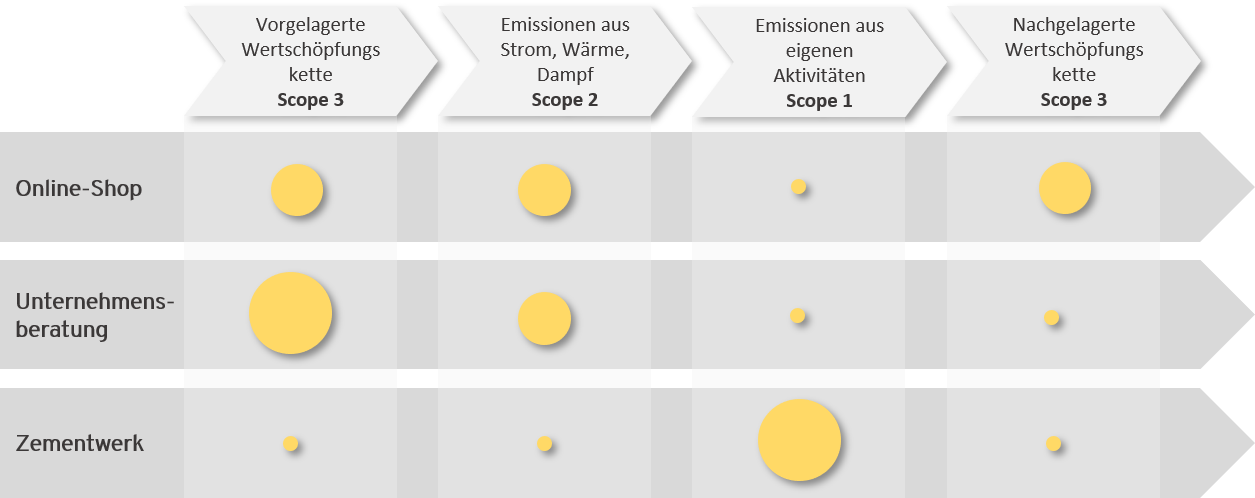

Operational system boundaries: Identify emission focal points in Scope 3

It is therefore important to make a brief qualitative assessment of the company's main emissions. (Where do most emissions occur? The categories that should be balanced are derived from the emission focal points. If high emissions are expected, these categories should be calculated in the company's carbon footprint. For example, the main emissions of an online shop in Scope 3 are in upstream and downstream logistics (3.4; 3.9) and in leasing server infrastructure (3.8), while for a consulting firm they are likely to be in business travel (3.6) and employee mobility (3.7).

Categories with expected low emissions do not need to be considered or are optional.

Tip: In the first year, data collection involves a lot of effort, so you should limit yourself to the most important (organisational and operational) categories and gradually expand the carbon footprint in subsequent years.

Anchoring the project organisationally

The company has now defined the system limits for the carbon footprint. This can be used to roughly estimate how much time and manpower is required. If the assessment is being carried out for the first time and only one main location is included and limited to the most important scopes, even in a medium-sized company with 500 employees, ¼ position over a period of 3 months may be sufficient. In any case, a coordinator should hold this position and be responsible for data procurement and collection. In the case of larger companies with differentiated legal and ownership structures and accounting for many categories, greater effort is to be expected. A small project team can be appointed in addition to a coordinator. In any case, it is advisable to assign the process to a responsible person or department in order to guarantee a smooth process.

3. collection and calculation of data for the company's carbon footprint

What data must be recorded and converted into CO2 equivalents?

Use existing data to measure the carbon footprint

The defined system boundaries in which emissions are to be measured show which activity and emission data must be collected. If no direct emissions data are available, these can be calculated from the activity data. Sometimes this is done by simple conversion, sometimes assumptions or estimates have to be made. This does not necessarily mean reinventing the wheel. What data is already available from existing management systems, controlling or tools? Even very simple data sources, such as invoices from energy suppliers, provide important data. The following list helps to get an overview of which systems in the company may already contain data for creating the carbon footprint.

Data sources for calculating CO2 emissions

- Controlling tools

- Management systems

- e.g. for booking business trips

- Invoices

- e.g. from energy suppliers

- Certifications and specific management systems

- CDP

- Ecoprofit

- Consultancy services

- Energy counselling

- Project participation

- LEEN - 30 pilot networks

- B.E.E. - Business Energy Efficiency Programme

- Other

- Participation in emissions trading - In this case, CO2 values from installations subject to emissions trading are already available.

Collecting and documenting data for the carbon footprint

The coordinator is now responsible for collating the data from the various departments and contacts. It is extremely helpful to use a standardised tool for this. On the one hand, CO2 calculators are a good option. We have tested and compared nine CO2 calculators for companies, read more here. However, the CO2 calculators often do not allow activity data to be recorded, which is why this data has to be collected internally elsewhere.

As simple as this may sound, a simple Excel spreadsheet is a good solution for recording the activity data, respective contact persons and assumptions made, even in large companies. For example, companies can record the data for Scope 2.1 "Emissions from purchased electricity":

Guaranteeing the quality of the company's carbon footprint

The collection and calculation of data for the company's carbon footprint is based on the principles of relevance, consistency, accuracy, transparency and completeness. However, experience shows that not all data is available in the appropriate quality. For example, for Scope 3.6 business trips, often only the travel expense reports are available without a breakdown of the kilometres travelled. It is common practice to convert the cost or financial activity data into emissions data using assumptions and estimates (e.g. total rail costs / average costs per rail journey * emissions factor per rail journey). In this case, the balancing is more complete, but also less accurate. Compiling the data therefore also serves to identify and close data gaps. To ensure quality, we always recommend documenting all assumptions made for the carbon footprint.

Calculate CO2 data

Once the activity data has been recorded, e.g. electricity in kWh, it is converted into CO2 equivalents. At best, this conversion is carried out using emission factors from scientifically recognised databases. The emission factors take into account the climate impact of the various greenhouse gases (global warming potentials).

Determine emission factors

In the case of electricity, for example, the emission factor of the electricity mix can be taken from the electricity bill, which the electricity supplier must disclose the amount of CO2 in grams or kilograms per kilowatt hour in accordance with Section 42 of the German Energy Industry Act (EnWG).

For other categories, such as Scope 3.6 business travel, scientifically calculated emission factors can be used. Common and recognised databases for emission factors on the German market are, for example GEMISwhich IPCC Guidelines and ProBas. For the calculation of Scope 1.3 emissions of volatile gases from air conditioning systems, for example, the Tools of the Greenhouse Gas Protocol.

For mobility data in Scope 1.2 Vehicle fleet and Scope 3.6 Business trips, such as the conversion of rail kilometres travelled into CO2 equivalents, the mobitool (ecoinvent) excellent.

Continuing and expanding the company's carbon footprint

For the successful continuation of the knowledge gained, it makes sense to document the survey, in particular via estimates and assumptions. This is entirely in line with the Greenhouse Gas Protocol principles, which, among other things, provide for consistency in the calculation of the corporate carbon footprint. Once the limits have been set, subsequent surveys should show the same framework conditions and procedures. If, for example, the calculation methodology changes due to an expansion of the accounting to include additional (significant) emission categories or due to better data quality, the company should also recalculate the base year if possible (if not, an explanation is required). This fulfils the requirement for a transparent, accurate and consistent comparison of CO2e emissions over time as well as between locations.

Conclusion

The CO2 balance summarises the emissions of a company. There are many ways and possibilities to carry out a carbon footprint. In order to achieve the goal successfully, we recommend preparing the carbon footprint assessment well in the first step by identifying targets and communicating the project internally. In the second step, the company defines the system boundaries for measuring the carbon footprint. This helps to ensure that the process runs smoothly, transparently and credibly. In the 3rd step, the data is collected and calculated. In addition to measurements and tools such as emission factors, estimates and assumptions may also be used. We strongly recommend documenting the data sources, assumptions, estimates, emission factors, etc. in order to ensure the quality and consistency of the calculations in subsequent years. As a result, the carbon footprint shows which areas of the company produce the most greenhouse gases. The carbon footprint thus reveals potential for minimising the company's climate impact and is therefore the most important basis for business decisions relating to climate protection.

Synonyms for a company's carbon footprint (or as a CO2 balancing process) are climate footprint, CO2 footprint of a company or corporate carbon footprint.

Are you planning the next steps towards sustainability?

Ask me for a free information meeting.

I am ready with advice and pleasure.

Franziska Kramer

Sustainability strategy and reporting topics

Methods and best practice for sustainability in your mailbox

[...] the measurement of the CO2 footprint, which identifies impacts and levers. Here we have simple instructions for calculating the carbon footprint [...]

[...] common tools. Alternatively, it can be implemented by external service providers. Here we have simple instructions for calculating the carbon footprint [...]

[...] and structural process steps. Read our blog article here for a step-by-step guide to creating a corporate carbon footprint. The steps are summarised briefly and concisely:1. management consensus on the project [...]

[...] the calculation of a carbon footprint, in the course of which the total emissions are recorded. In our blog post "3 steps to a carbon footprint in companies", we explained how this is created. On the basis of the empirical results, [...]

[...] This requires the necessary human resources to familiarise the person responsible with the subject area. In order to create a good and credible carbon footprint, you need expertise in recognised standards (e.g. Greenhouse Gas Protocol or ISO 14064) and process knowledge. Process knowledge includes knowing where and how to obtain which data in the company and how it can be scientifically converted into CO2 equivalents. If sufficient time and human resources are available, nothing stands in the way of the company carrying out its own carbon footprint assessment. We have compiled a guide to this in our blog article 3 steps to a CO2 balance sheet in the company. [...]

[...] Change in car policy with a changed focus on CO2 data for combustion engines (https://www.mobilitypolicy.de/). On the one hand, lower CO2 emission values can be rewarded with a higher budget. On the other hand, the time spent travelling by different means of transport can be assessed differently. This is because routine or idle work such as expense reports or documentation can be processed on the train, while full attention must be paid to travelling by car. Travelling time by train could be weighted more with a factor of 0.75 than, for example, recording working time in the car with a factor of 0.25. Further information on the CO2 balance in the company here. [...]

[...] In previous articles, we have already looked at how companies can systematically determine their carbon footprint, which key questions should be answered and which tools can be used to [...]

[...] In our blog article "3 steps to a carbon footprint in your company", we explain the procedure for creating a carbon footprint [...]

[...] are. The basis for this is a materiality analysis. A partial element of this can also be a carbon footprint. A materiality analysis analyses the entire value chain, [...]

[...] We have prepared the greenhouse gas balance for 2023 in our own Excel tool in accordance with the international Greenhouse Gas Protocol standard, taking into account all relevant greenhouse gases. These are also called CO2 equivalents or CO₂e. (read more about 3 steps to a carbon footprint here) [...]